CSL An Exercise In Wealth Destruction

Markets broadly operate in two dominant phases: wealth creation and wealth destruction. Too often, investors and traders fail to participate fully in the former, only to allow the latter to devastate whatever gains they may have made. Such a situation is unfolding on the ASX at present with CSL.

For decades, CSL was viewed as one of the ASX’s untouchable “quality” stocks:

- Dominant global market position,

- Strong margins,

- Healthcare defensiveness,

- Elite management,

- Long history of price appreciation.

Over time, investors stopped treating CSL as a position and began treating it as a permanent holding. It was viewed as a set and forget investment that would always go up – this was certainly the view of the stockbroking fraternity that relentlessly marketed CSL as being “safe”

The most dangerous losses often occur not in speculative assets but in assets that investors emotionally classify as “safe.”

The fairy tale began to unwind in 2021 with the acquisition of Swiss renal therapy company Vifor Pharma. An acquisition that will undoubtedly go down in history alongside massive corporate cock ups such as Alan Bond’s purchase of the Nine Network for $1B. Although CSL has $5B USD in write-downs so far, its management makes Bond look like an amateur.

The infographic below tells the story of the Vifor debacle.

What is interesting about this situation is that it is a case study in many of the mistakes that investors make and the psychology behind those decisions. The chart below shows CSL’s YTD drawdown.

As can be seen, the stock is down some 44.96% YTD – this does prompt the question as to why investors didn’t start to sell as the price began to slip precipitously. The answer to this is probably tied to a few factors.

As can be seen, the stock is down some 44.96% YTD – this does prompt the question as to why investors didn’t start to sell as the price began to slip precipitously. The answer to this is probably tied to a few factors.

Narrative Inertia

For decades, the prevailing narrative surrounding CSL was extraordinarily powerful:

- World-class management,

- Predictable growth,

- Defensive earnings,

- Long-term compounding.

Narratives persist long after conditions begin changing.

This causes investors to reinterpret deteriorating price action not as a warning, but as an opportunity to reaffirm existing beliefs. The stronger the prior narrative, the harder it becomes psychologically to recognise that the underlying conditions may have fundamentally changed.

Loss Aversion

Human beings experience losses asymmetrically.

The pain associated with crystallising a loss is substantially greater than the pleasure associated with an equivalent gain.

This often causes investors to:

- Hold deteriorating positions,

- Avoid acting decisively,

- Rationalise weakness,

- And wait for “just a bounce.”

What begins as a manageable decline can gradually evolve into catastrophic capital destruction.

Institutional Inertia

Large institutions are often structurally slow-moving.

Many funds owned CSL because it was:

- Liquid,

- Benchmark relevant,

- Institutionally respected,

- Historically dependable.

The larger and more widely accepted the position, the more psychologically and operationally difficult it becomes to exit early. Institutional ownership can therefore amplify wealth destruction rather than prevent it.

However, it is worth noting that CSL reached its all-time high in 2020 and, until the latest decline, had been trading sideways.

The most overlooked aspect of these sorts of falls is that they not only destroy wealth but also destroy time. The chart below shows that if you had invested $10,000 into CSL ten years ago, you would now have $10,362. Many long-term CSL investors have effectively lost close to a decade of capital appreciation.

This matters enormously because compounding is path dependent.

This matters enormously because compounding is path dependent.

Capital trapped recovering old losses is no longer compounding into new opportunities. It is merely attempting to return to break-even. If we make the very broad assumption that the average entry price over the past five years was $250, then the price will need to increase by 153.7% to break even. If I were unfortunate to buy it at its peak in 2020, then the price will have to gain 216% to break even.

In writing this, I am reminded of the following from the humourist Dave Barry.

Q: Why didn’t Wall Street realise that Enron was a fraud?

A: Because Wall Street relies on stock analysts. These are people who do research on companies and then, no matter what they find, even if the company has burned to the ground, enthusiastically recommend that investors buy the stock.

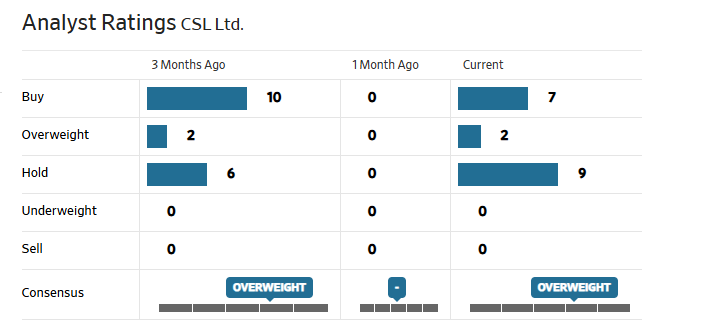

This raises the question as ot the role of the advisory industry in pushing stocks that are clearly collapsing. The table below is from the Wall Street Journal and compares analysts’ ratings for CSL three months ago, when the price was hovering around g the $150 mark, and now. As you can see, it was even recommended to halve. I imagine they guessed that it couldn’t halve again.

Also interesting are the widely inaccurate price forecasts by analysts, as shown in the image below.

This does raise the question of what lessons can be drawn from such a collapse. From my perspective, the answer is simple – play defence. CSL has been a bust from 2020 – if your long-term stock holding is not making new highs, then it should be consigned to the scrap heap, and you move on and find something else. Stories don’t matter.

It is also a lesson on the broader issue of wealth destruction. Wealth destruction is not simply falling prices.

It is the destruction of:

- Capital,

- Opportunity,

- Confidence,

- Time itself.

And for many investors, time is the one asset that cannot be recovered.

Team that up with COH, XRO, PME together with a few others from the top 100 and your portfolio would be look rather dismal at the moment.

You could probably add CBA and NAB to that list.

Thank you Chris, another lesson in why the study is psychology with trading matters!

👍