The Natural Gas Paradox

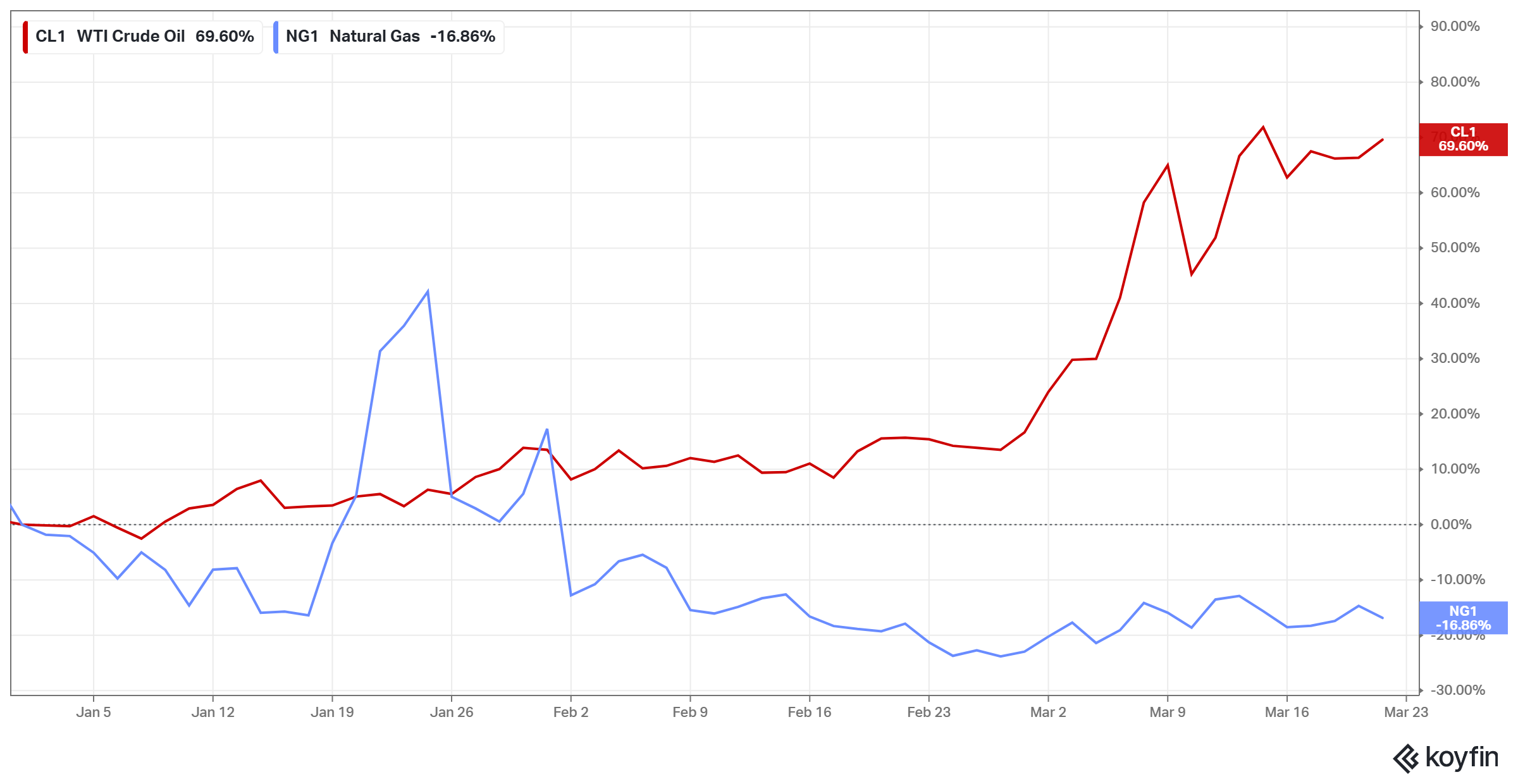

The chart below is a year to date comparison of crude oil and natural gas.

What is immediately apparent is the performance differential between the two since the start of the latest conflict in the Middle East. This is interesting because superficially, when we view commodities within a given sector, we tend to think of them as being uniform. So the narrative that arises is that energy supplies have been disrupted, and all energy commodities should be going up.

What is immediately apparent is the performance differential between the two since the start of the latest conflict in the Middle East. This is interesting because superficially, when we view commodities within a given sector, we tend to think of them as being uniform. So the narrative that arises is that energy supplies have been disrupted, and all energy commodities should be going up.

The March 18, 2026, ballistic missile strike on Ras Laffan Industrial City in Qatar was supposed to be the “Armageddon” moment for the global natural gas market. With 19% of global liquefied natural gas (LNG) supply effectively severed overnight and QatarEnergy declaring force majeure on its long-term contracts, many observers expected gas prices to mimic the parabolic upward trajectory of crude oil, which had already tested $120 per barrel.

The March 18, 2026, ballistic missile strike on Ras Laffan Industrial City in Qatar was supposed to be the “Armageddon” moment for the global natural gas market. With 19% of global liquefied natural gas (LNG) supply effectively severed overnight and QatarEnergy declaring force majeure on its long-term contracts, many observers expected gas prices to mimic the parabolic upward trajectory of crude oil, which had already tested $120 per barrel.

However, as with all things related to markets, there is much nuance to be had.

The Simplistic Narrative: The “Parallel Shock” Theory

![]() The simplistic expectation was rooted in the crisis’s shared geography. Because the Strait of Hormuz serves as the primary artery for both 20% of global oil and 20% of global LNG, it was assumed that a maritime blockade would trigger a symmetrical price shock. When Iranian strikes successfully degraded the infrastructure at Ras Laffan—knocking out 17% of Qatar’s capacity for an estimated three to five years—the case for triple-digit gas price surges seemed a lock.

The simplistic expectation was rooted in the crisis’s shared geography. Because the Strait of Hormuz serves as the primary artery for both 20% of global oil and 20% of global LNG, it was assumed that a maritime blockade would trigger a symmetrical price shock. When Iranian strikes successfully degraded the infrastructure at Ras Laffan—knocking out 17% of Qatar’s capacity for an estimated three to five years—the case for triple-digit gas price surges seemed a lock.

On the surface, this is a reasonable narrative, since gas is often considered crude’s “brother.” Based on this, the obvious trade would be long gas; however, remember that there is more than one narrative in the market, and it votes on what it considers the best one. And this narrative is reflected in price.

The alternative narrative wasn’t immediately obvious to me since I am not a macro analyst, so I had to do a bit of digging to get a sense of the bigger picture regarding gas.

Reality Check 1: The Pre-War Supply Buffer

One of the most significant differentials was the starting position of each market. Before the conflict began, the global oil market was already operating with thin spare capacity, primarily concentrated in Saudi Arabia. In contrast, the LNG market was entering what analysts called an “unprecedented expansion” and a projected period of significant oversupply.

In simple terms, oil is in short supply, and gas is in surplus. This existing glut acted as a massive shock absorber, allowing the market to lose Qatari volumes without immediately descending into a physical shortage—a luxury the oil market, which had to shut-in 9 million b/d of production due to storage saturation, did not have.

Reality Check 2: The “Relief Valve” of US Contract Flexibility

The two markets differ sharply in their logistical elasticity. The Qatari LNG model was historically defined by rigidity: multi-decade contracts with fixed destinations and little room for diversion. When Ras Laffan was hit, these flows simply stopped, creating a “single-point failure” for its primary Asian buyers.

The U.S. LNG model, however, provided a global “relief valve.” Approximately 75% of new U.S. supply features flexible destination clauses, allowing traders to rapidly re-optimise their portfolios. As the Qatari volumes vanished, traders redirected flexible Atlantic cargoes to Asia to fill the gap. While this created a scramble for spot cargoes, it prevented the total supply chain paralysis seen in the regional crude trade, where VLCC (Very Large Crude Carrier) charter rates soared by 400% as tankers became stranded behind the blockade.

Reality Check 3: Demand Destruction and Regional Decoupling

The natural gas market has also shown a greater capacity for “fuel switching” than the transportation-heavy oil market. Faced with immediate price spikes—Asian LNG benchmarks jumped 40% at the start of the war—price-sensitive emerging economies like India, Indonesia, and Bangladesh did not just pay more; they switched back to cheaper indigenous coal for power generation.

Reality Check 4: The Mismatch in Pricing Timelines

Finally, there is a psychological differential in how the markets perceive the “end-game.” Crude oil prices reacted to the immediate physical loss of transit through Hormuz. For natural gas, however, the consensus until mid-March was that the disruption would be limited to a two-month “quick fix”.

When we synthesise all this, we get two competing narratives, the endpoints of which are reflected in the price of natural gas.

Whilst the above points sound impressive as narratives for and against a rise in the price of natural gas, there are three important considerations.

1. There are always people who think differently from you.

2. The markets’ vote on price might not be the same as yours.

3. Everything is reflected in price – you just have to listen to what it is saying rather than what you think it should say.

Good article and excellent 3-point conclusion.

I might add that in general LNG companies contract structures limit their ability to capture spot price gains. LNG companies typically have a large percentage of use-or-pay contacts. Buyers must pay for contracted volumes even if they cannot take delivery-but the Hormuz crisis has disrupted actual volumes. These contracts are designed to give LNG companies stable cash flow. LNG Exporters using Hormuz for now cannot supply their contracted volumes. Even if they were to ‘book’ the contracted revenues without receiving the cash they would have to supply the contracted volumes in the future. Also LNG does not have equivalent strategic stockpiles as it must be moved from the liquification plant to the buyer continuously, directly by pipeline, or by pipeline onto ships.

Most LNG exporters have contract structures heavily weighted to stable cash flows but limited upside from price spikes.