Great Stocks, Bad Entries

Technical analysis has long treated entry precision as sacred. Traders spend careers searching for the perfect breakout, the ideal pullback, the exact moment of volatility contraction.

But what if the entire premise is wrong — and traders have been optimising the wrong variable all along?

The Core Assumption

It has always been assumed that a superior entry in terms of timing leads to markedly superior results. This belief consumes an enormous amount of effort among traders, who are perpetually trying to refine their timing and hunt for better entries, all in the hope of finding perfect conditions before committing to a trade.

But this raises a question – what happens to the end result if the entry is less than perfect? Does a less than perfect entry completely collapse the return from the trade, or does it simply put a small wrinkle in overall performance?

To try to answer this question, I generated a collection of exceptionally long-term winning stocks from both the United States and Australia. Rather than optimising entries, researchers asked a more fundamental question: Are outstanding stocks forgiving of imperfect timing?

To do this, I used the following small universe of stocks –

Methodology

Methodology

Signals were defined using a simple, objective, and replicable rule: buy the first close above the previous 100-day high. There is nothing special about the number 100 – it is just a number I picked at random. It could be any breakout period. So, before everyone rushes off to change whatever breakout period they have to 100, just remember that.

There is a simplicity in clean breakout triggers that requires no discretionary interpretation, making it suitable for systematic comparison across multiple stocks and time periods. Five distinct entry scenarios were then tested, deliberately staggering entries from the breakout day itself out to forty full trading days later. Twelve-month returns were measured from each entry point, providing a consistent holding period across all scenarios.

The design is intentionally simple. Whilst complexity in methodology is always attractive to traders, it can obscure the question you are trying to answer. By keeping the signal and the measurement period constant while varying only the entry timing, the study isolates the precise variable under investigation: does it matter when you get in, relative to a defined breakout signal?

The Results

Whenever you have consistent results in any form of study, there are two possible reasons for this: you have either made a mistake somewhere or the results are correct. To make certain I hadn’t made a silly error, I reran the data numerous times, making subtle tweaks in the breakout periods. The same pattern asserted itself across breakouts.

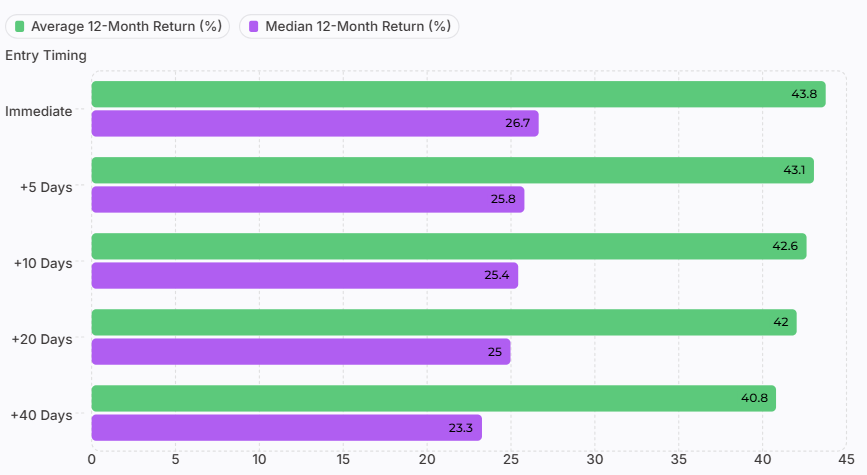

Entering forty trading days late — two full calendar months after the breakout signal — reduced average twelve-month returns by less than three percentage points. The degradation across all five scenarios was gradual, orderly, and surprisingly small. This suggests that powerful trends are not merely forgiving of poor entries — they are remarkably, almost stubbornly, tolerant of them.

The quality of the trend driving the stock appears to be the dominant driver of returns, with entry timing playing a secondary — almost marginal — role across the one-year holding horizon. This finding directly challenges the conventional wisdom that obsessive attention to entry precision is the path to superior performance.

The Cost of Waiting for Perfection

There is a secondary question that flows naturally from the observation that being late doesn’t materially harm performance in stocks that are trending well.

Perhaps waiting for a meaningful pullback is a superior strategy?

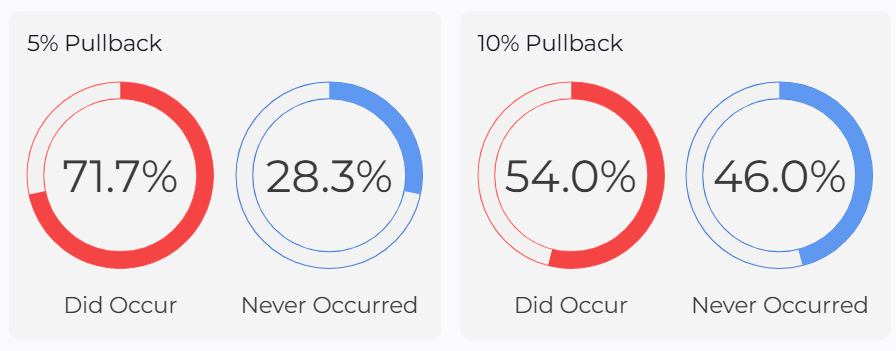

To answer this, every breakout was examined to determine whether a 5% or 10% retracement eventually occurred after the initial signal. The results expose a critical and widely overlooked reality: a significant proportion of the strongest trends never offered traders the pullback they were waiting for.

Patience, in these cases, was not rewarded — it was penalised.

Nearly one-third of opportunities never produced a 5% pullback. Almost half never produced a 10% pullback. For traders whose discipline requires buying weakness, this data reveals that such a strategy structurally excludes a large subset of the most powerful trending opportunities — not because of bad luck, but because the strongest stocks simply refuse to cooperate.

Simple conclusion – buy the friggen stock when it breaks out dont dick about thinking how clever you will look if you manage to get it on a pullback.

Time to Pullback

For those trades where a pullback did eventually materialise, the waiting period itself carries an often-overlooked cost: time. While the trader waits on the sidelines for the stock to retrace, capital sits idle, and opportunity cost accumulates. The median wait for a 5% pullback was 16 trading days — roughly three weeks. For a 10% pullback, the median extended to 36 days.

The Cost of Waiting

The notion of an opportunity cost is somewhat abstract and is difficult for traders to fully grasp. To overcome this, I needed to quantify the impact of missed trades.

Those where the pullback never arrived were assigned a return of zero. This is a conservative and realistic assumption: a trader waiting for a retracement that never comes simply does not participate in that move. The results are striking and serve as a powerful corrective to the intuitive appeal of waiting to buy dips in strong trends.

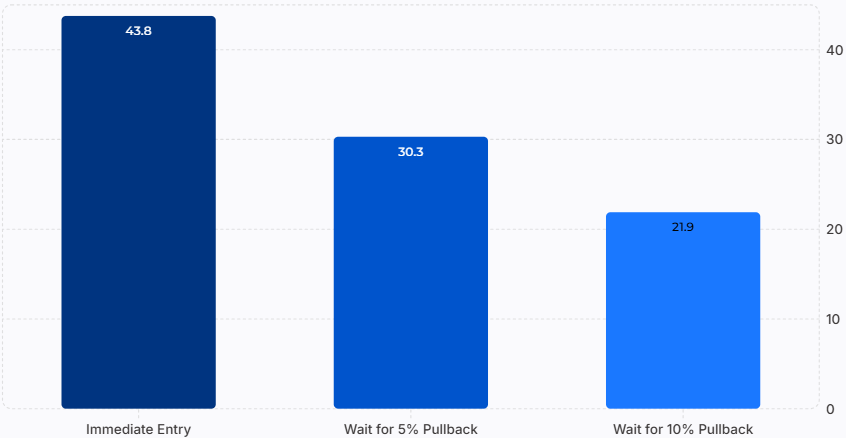

Waiting for a 5% correction shaved more than 13 percentage points off the average annual return compared to immediate entry. Waiting for a 10% correction cuts average returns almost in half.

The irony is acute: the very discipline intended to improve the quality of entries ends up dramatically reducing the strategy’s overall return. The strongest stocks frequently denied traders the “perfect” entry.

The Trades That Never Pulled Back

What I found most interesting in the exercise is the subset of trades that never provided a meaningful pullback. Rather than simply being the “unlucky” trades that got away, these turned out to be the most powerful performers in the dataset — by a considerable margin. The very stocks that refused to give traders a second chance were, in aggregate, the best stocks in the study.

The trades with no 5% pullback delivered an average 12-month return of 81.5% — nearly double the overall study average of 43.76%. These were not merely good trades; they were exceptional ones. The implication is uncomfortable but important: a strict pullback-entry discipline doesn’t just miss some trades. It systematically excludes the very best ones. In other words, the market rarely rewards perfection. It rewards participation.

Is It Just Nvidia and Pro Medicus?

An obvious and very legitimate criticism of the study’s aggregate findings is that a handful of extraordinary performers may be distorting the entire dataset. If two or three exceptional outliers are driving the average returns, the conclusions would be far less generalisable.

Strong contributions came from technology stocks, healthcare businesses, consumer companies, Australian names, and American names across different decades. The phenomenon of trend forgiveness appeared broadly and consistently across the dataset.

This breadth suggests that the basic finding — that exceptional trends forgive imperfect entries — reflects a structural characteristic of powerful trending markets, not just the statistical distortion created by one or two spectacular outliers.

Position Section vs Entry Precision

My view is that there is a clear hierarchy of importance in the trading process. This hierarchy does not diminish the value of entry work — but it does reframe where that work belongs in the overall priority structure of a systematic trading approach. Understanding this distinction has significant implications for how traders allocate their time and cognitive resources.

Position Selection Determines Returns

Exceptional trends create exceptional outcomes. No amount of entry optimisation can transform a mediocre trend into a great one. The decision of which stock to own is the primary driver of long-term portfolio performance. This is where the most significant leverage lies for the active trend follower.

Entry Quality Determines Efficiency

Good entries improve position sizing, drawdown management, and psychological comfort during a trade. These are real and meaningful benefits. But they do not appear to generate returns — rather, they enhance and refine the returns generated by the stock itself.

To put it into a current context. Position selection is a variation of right market, right time. You can be the best stock picker in the world, but if you are in the wrong market, it doesn’t matter how good you are; you cannot generate returns from your positions if they are not there to be had.

As an example, consider two competing traders from 12 months ago – one is convinced that the domestic banking sector is about to go on a tear. The other is convinced that AI is the next big thing in markets. They are both equally skilled.

Fast forward 12 months, and it is clear who will be the winner. The trader committed to AI could have thrown darts at a list of names and still achieved superior performance. Right market – right time.

Risk Matters

So far, I have avoided the question of risk because it is a difficult one to answer. My observation is that stocks that trend powerfully forgive late entries over a 12-month period. However, poor entries are unlikely to be equally forgiving from a risk perspective.

A trader who enters forty days late in a strongly trending stock may capture nearly the same annual return — but may do so with a materially larger drawdown along the way, simply by virtue of having paid a higher price relative to the earlier entry price.

Position selection determines whether you make money.

Entry quality determines how comfortably you make it.

This is not to diminish the notion of a “good” entry.

Good entries may therefore improve maximum adverse excursion, overall R return, achievable position size, and emotional comfort during the holding period — all of which have real practical value for a trader.

The Psychological Trap

Many traders spend years waiting for perfection. The discipline of buying weakness is, on the surface, a sound and intellectually appealing approach. It speaks to the professional instinct to avoid chasing, to be patient, to wait for better prices.

You are waiting for a bargain. Intriguingly, the psychology that stops traders from pyramiding into winning positions is the same as the one that causes them to wait for pullbacks. It is a perception of cost and, in turn, relative value. If the stock is $5.00 today, maybe if I wait a bit, it will be $4.50.

Counterpoints

I alluded to the notion of this being a biased sample, and that is a valid observation. However, it is important to understand what this little experiment was asking and what it wasn’t.

It doesn’t claim that bad entries don’t matter, nor does it claim that you can buy anything late and do well, and it doesn’t claim that stock selection doesn’t matter.

The study specifically targeted winners, and that was a deliberate choice as we are not interested in how average performing stocks behave. The question was among the leading ones in the market segment: how much does entry precision matter?

I think the same answer applies to the criticism of survivor bias. And it is a survivor bias dataset, but it has to be because I am interested in survivors – I want to know what properties are common to strongly trending stocks, not what the average behaviour of all stocks is.

The Bigger Point

Traders spend an enormous amount of time trying to perfect their entries, but no matter what precision you bring to bear, you cannot transform a lagging sector or a non-trending stock.

To use another historical example, a perfect entry into Kodak does not make Kodak into NVIDIA.

However, I am not saying that entry skills don’t matter. I think it is more nuanced to say that the stronger the underlying tone of a given segment/industry, the less important the entry becomes.

If the underlying trend is febrile, as it is in the stocks I looked at, then the trend is surprisingly forgiving of a late entry. If the underlying trend is lacklustre, then entry precision has to do a lot of heavy lifting, and even then it won’t compensate for being in the wrong market segment.

Simple conclusion – buy the friggen stock when it breaks out dont dick about thinking how clever you will look if you manage to get it on a pullback.

I like that summary for my revision notes.